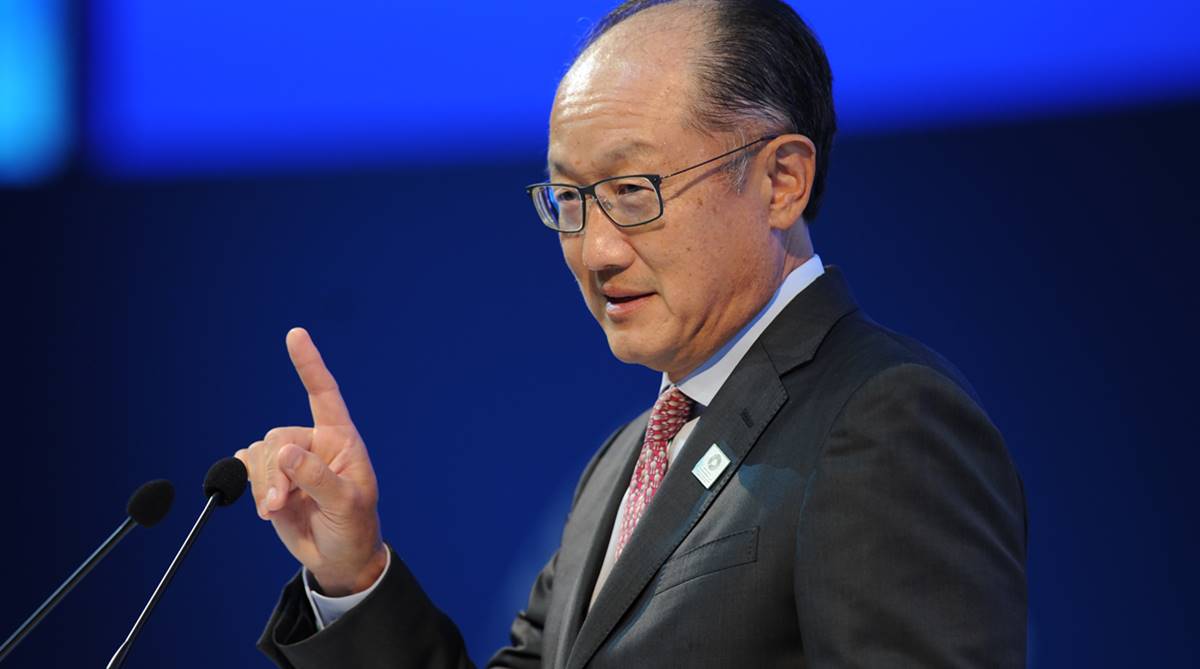

In a surprise move, World Bank President Jim Yong Kim announced on Monday that he would step down from his position on February 1 much before the end of his term in 2022.

Kim, 58, has been in this position for over six years now.

Advertisement

The president of the Washington-based World Bank has always been an American citizen nominated by the United States, which is the largest shareholder of this multilateral financial institution.

“It has been a great honour to serve as President of this remarkable institution, full of passionate individuals dedicated to the mission of ending extreme poverty in our lifetime,” Kim said.

Kristalina Georgieva, World Bank CEO, will assume the role of interim President effective February 1.

“The work of the World Bank Group is more important now than ever as the aspirations of the poor rise all over the world, and problems like climate change, pandemics, famine and refugees continue to grow in both their scale and complexity,” Kim was quoted as saying in a World Bank press release.

“Serving as President and helping position the institution squarely in the middle of all these challenges has been a great privilege,” he said.

During his term as World Bank President beginning July 2012, Kim emphasised that one of the greatest needs in the developing world is infrastructure finance and he pushed the Bank Group to maximize finance for development by working with a new cadre of private sector partners committed to building sustainable, climate-smart infrastructure in developing nations, the release said.

To that end, Kim announced that, immediately after his departure, he will join a firm and focus on increasing infrastructure investments in developing countries, it said, adding that the details of this new position will be announced shortly.

Under his leadership, the World Bank established two goals: to end extreme poverty by 2030; and to boost shared prosperity, focusing on the bottom 40 percent of the population in developing countries. These goals now guide and inform the institution in its daily work around the globe, it said.

In addition, shareholders strongly supported measures to ensure that the Bank Group be even better positioned to respond to the development needs of clients:

The Bank Group’s Fund for the Poorest, IDA, achieved two successive, record replenishments, which enabled the institution to increase its work in areas suffering from fragility, conflict, and violence.

In April 2018, the Bank Group’s Governors overwhelmingly approved a historic USD 13 billion capital increase for IBRD and IFC that will allow the Bank Group to support countries in reaching their development goals while responding to crises such as climate change, pandemics, fragility, and underinvestment in human capital around the world.

“Over the past 6+ years, the institutions of the World Bank Group have provided financing at levels never seen outside of a financial crisis, the bank said.

Recognising the power of capital markets to transform development finance, the Bank Group during Kim’s tenure also launched several new innovative financial instruments, including facilities to address infrastructure needs, prevent pandemics, and help the millions of people forcibly displaced from their homes by climate shocks, conflict, and violence.

The Bank is also working with the United Nations and leading technology companies to implement the Famine Action Mechanism, to detect warning signs earlier and prevent famines before they begin.